Choosing the trail: Strategic selection of forensic accounting tracing methods

27th February 2026

As a father of twins, I’m often confronted with a quandary when preparing their last meal of the day. Will the decision to choose a sugary dessert for my five-year-olds end up hurting me several hours later, when they are treating their bedroom like a dance club? Am I choosing the path of least resistance, failing to properly evaluate nutritious food options, and thereby undermining my credibility as a father? This decision-making process is similar to one faced by forensic accountants when deciding which method(s) to use in conducting a flow-of-funds tracing analysis on behalf of a client.

In my 2024 article titled “Following the Money: Forensic Accounting Tracing Methods & Best Practices,” I conducted a deep dive into forensic accounting tracing methods and identified the four best-known methods — first in, first out (FIFO); last in, last out (LIFO); pro rata; and the lowest intermediate balance rule (LIBR). Now, I want to analyze when and why forensic accountants should use these methods to conduct a funds tracing analysis.

It is not enough to simply understand how each method can be applied in principle. There are several factors to consider. As defined by the American Institute of Certified Public Accountants (AICPA), when performing forensic services, certified public accountants (CPAs) are guided by principles such as professional competence, integrity and objectivity, and due professional care. The end goal of selecting a tracing method(s) for use in a tracing exercise should be considerate of the client’s identified scope, but not at the cost of the forensic accountant’s credibility and ability to analyze the facts of the case.

As discussed in “Following the Money,” there is very little legal precedent explaining why or how the court has approved certain tracing methods. Here, I analyze how forensic accountants select an appropriate method using a defined set of facts. Although the AICPA and other organizations, such as the Association of Certified Fraud Examiners (ACFE), provide general guiding principles for forensic accountants, no detailed blueprints exist. Due to this ambiguity, the tracing exercise can be cumbersome, albeit necessary, when used alongside the presentation of an expert opinion.

Analyzing the facts of the case

The forensic accountant must consider all available tracing methods when performing a tracing analysis. Observing the AICPA principle of due professional care, it is insufficient to arbitrarily select a method(s). Instead, the selection process should first evaluate each of the four methods. When the analysis of the methods compared to the facts and patterns of the case is complete, the tracing exercise can begin.

So, how do we make that determination? How can we abide by these guiding principles while also serving as arbiters of which method(s) to include or exclude? The forensic accountant must not only make this decision but also provide context for why the selected method(s) were chosen. Consider the following scenario:

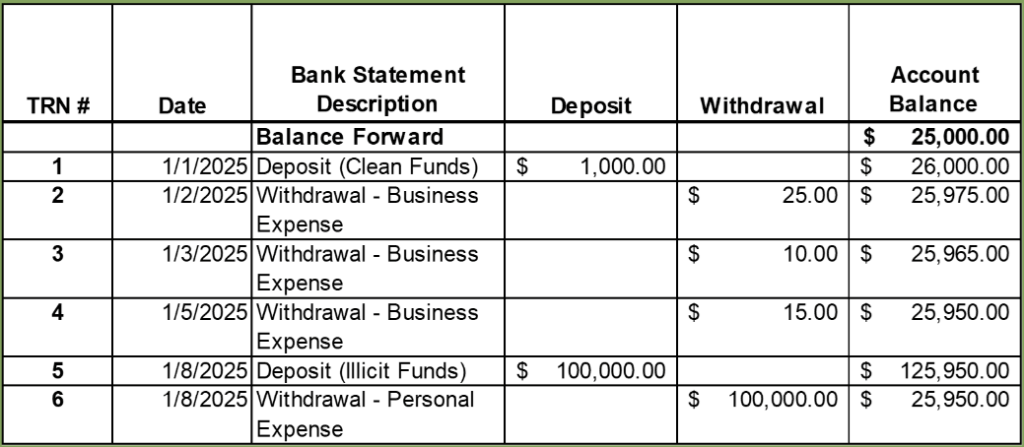

In this scenario, the bank account analyzed has a balance of $25,000 as of January 1, 2025. Over the next few days, an additional $1,000 of clean funds is added to the account, and withdrawals are made for business expenses of $25, $10, and $15. On January 8, the account is now commingled with a $100,000 deposit of illicit funds. The same amount of money is then immediately withdrawn for a personal expense, leaving the account balance at $25,950.

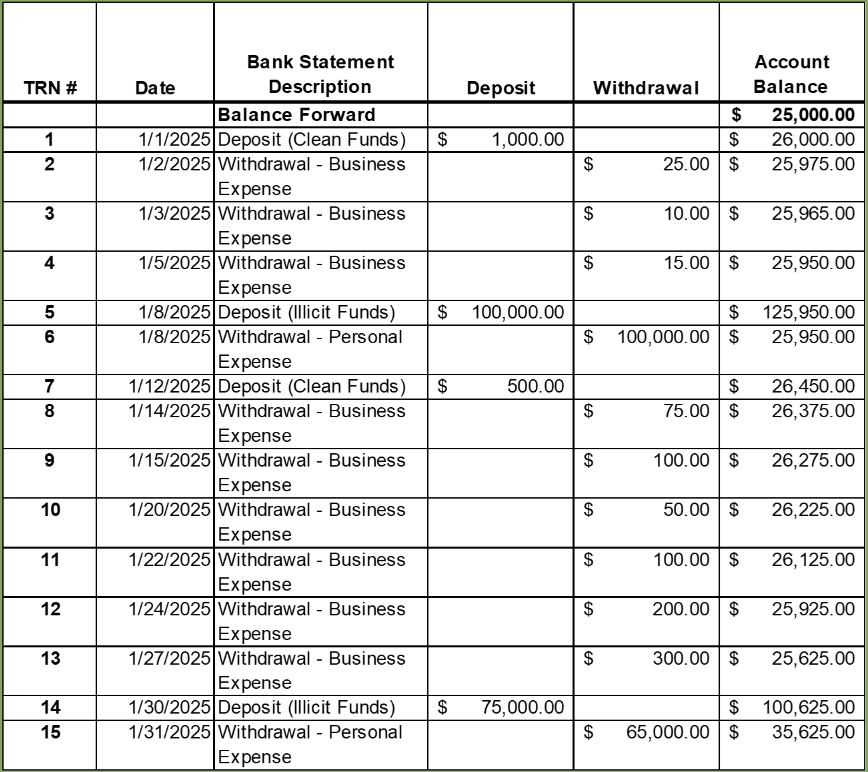

Let’s now review the rest of the account’s activity for the month of January 2025:

It doesn’t take an accounting or fraud examiner background to assess the flow of funds in this bank account. The account can pay minor business expenses using the clean funds account, but as soon as it receives funding from ill-gotten sources, the money is immediately used to pay a personal expense. So, now comes the decision: Which method(s) should be applied to this set of transactions to conduct a credible, thorough tracing analysis?

Let’s evaluate each of the four accepted tracing methods: FIFO, LIFO, pro rata, and LIBR. Because FIFO and LIFO can be considered more uncompromising measures of tracing,[1]Robinson, Marylee, and Wright, Jason. (2018, September). “Examining the most commonly accepted equitable tracing methods in bankruptcy proceedings.” ABI Journal, XXXVII (9). beginning with these methods makes sense. From the pattern of the illicit funds being immediately transferred out, it is reasonable to assume that, in this scenario, as LIFO dictates, the last funds to enter the account are attributable to the first funds to exit, providing a rationale for selecting the LIFO method over FIFO.

Pro rata and LIBR are sometimes held in higher regard by the courts as they rely less on the specific timing of the bank account’s transactions. These methods offer greater flexibility but pose potential risks to the validity of the tracing analysis if not applied correctly. LIBR tracing, in particular, can create issues for the forensic accountant because this method is often seen as a benefit to the accused party, as the illicit funds are “preserved” in the account until all clean funds have been spent. Pro rata, however, analyzes the account on a rolling basis and should almost always be considered in a tracing exercise as a method the forensic accountant would consider.

Selecting the appropriate tracing method

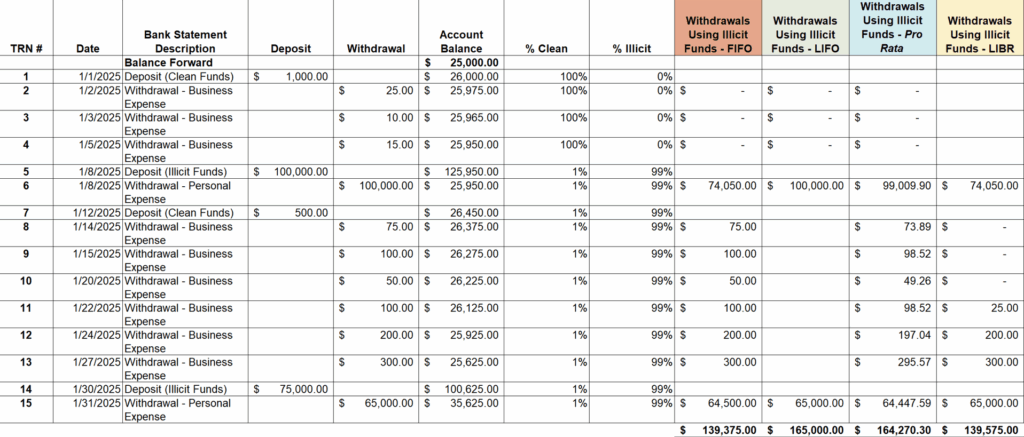

For purposes of this example, let’s assume each method was used by the forensic accountant. Following, we can see the total illicit funds withdrawn from the account by method:

It might be tempting for the forensic accountant to choose the FIFO method in the tracing analysis shown above. It would certainly make for an easier conversation, as the FIFO result shows the fewest illicit withdrawals among the other methods. Although choosing FIFO in this scenario may be tempting, let’s take a more detailed look at the tracing analysis itself to test the appropriateness of the methods.

When looking at the $100,000 withdrawal on January 8, 2025, and the $65,000 withdrawal on January 31, 2025, it should be noted that both withdrawals for personal expenses occurred immediately after deposits of illicit funds. This fact pattern would lend itself to a LIFO rather than a FIFO pattern, as the withdrawals nearly matched the deposits that preceded them, which is evidence of the LIFO principle. While that conversation with the client may be more challenging if LIFO is selected, it creates a level of trust and neutrality in the forensic accountant’s tracing analysis that is much more likely to hold up in litigation.

Alternatively, the forensic accountant may choose to present a range of outcomes. In this set of facts, it may be useful to present LIFO and another method. This is where less rigid pro rata and LIBR methods come in. The LIBR method in this scenario offers an alternative analysis and yields a lower amount, which is a good reason for the forensic accountant to choose both LIFO and LIBR methods in this tracing exercise when providing an opinion.

A thorough process behind selecting a method(s) is necessary. However, the forensic accountant must also ensure professional standards are followed when performing the tracing exercise.

Professional standards and expectations guiding method selection

As discussed in “Following the Money,” there is no established legal standard or authoritative guidance from organizations such as the AICPA and the ACFE prescribing a single process or method for forensic accountants to use when conducting a tracing analysis. In the absence of such direction, existing principles are essential for guiding forensic accountants in both the analysis and the selection of appropriate tracing methods.

Although no dedicated standard governs the method selection process, the AICPA provides broader forensic services guidance that outlines key principles relevant to this work, including the following:

- Professional competence

- Integrity and objectivity

- Due professional care

- Adequate planning and supervision

- Use of sufficient relevant data

- Proper communication with clients[2]AICPA FVS SSFS No. 1. Available at: Statement on Standards for Forensic Services | Resources | AICPA & CIMA

The Statement on Standards for Forensic Services (SSFS) No. 1, released by the AICPA’s Forensic and Valuation Services (FVS) Executive Committee on January 1, 2020, is one of the foremost standards relied on by CPAs when performing services that meet the definition of forensic or litigation services. While CPAs previously relied on broad standards applicable to all accountants, SSFS No. 1 provides guidance tailored to forensic engagements. Additionally, SSFS No. 1 removes uncertainty about how forensic accountants are compensated for their work and the types of opinions they can provide in court.[3]Duffus, David. (2019, August 27). “Overview of the statement on standards for forensic services.” Baker Tilly website. Available at: … Continue reading

No one-size-fits-all approach

The forensic accountant’s greatest asset when providing an opinion on the selection of tracing methods is their impartiality and objectivity. To determine the appropriate approach in any tracing exercise, the forensic accountant must prioritize integrity and neutrality while remaining attentive to the facts of the case and the patterns within the bank account activity. A thorough, case-specific process is essential (even when the forensic accountant must be mindful that each tracing analysis performed is not identical). In the world of funds tracing, these considerations strengthen the forensic accountant’s credibility and help ensure the court’s confidence in the expert’s testimony on tracing method selection. In the world of parenting, however, results may vary.

About the author

Jordan Sandberg, CPA, CFE, is a forensic accountant and investigator with over eight years of experience in dispute resolution. With a focus on forensic accounting, financial investigations, commercial damages, and valuations, he has assisted government and private-sector attorneys in multiple investigations to help them identify and trace ill-gotten gains from various fraudulent schemes. Contact Jordan at jordansandberg@hka.com.

This article presents views, thoughts or opinions that are provided for general information purposes only. It does not represent the views of, or constitute advice of any form (legal, professional or otherwise) from, HKA or any of its affiliates. While HKA takes reasonable care to ensure the accuracy of its contents at the time of publication, the article does not deal with all aspects of the referenced subject matter and may not be relied upon as a substitute for professional judgement or independent analysis. Accordingly, neither HKA nor the author accepts liability for any use of, or reliance on, the information presented in the article. This article is protected by copyright © 2026 HKA Global, LLC/© 2026 HKA Global Ltd. All rights reserved.

References

| ↑1 | Robinson, Marylee, and Wright, Jason. (2018, September). “Examining the most commonly accepted equitable tracing methods in bankruptcy proceedings.” ABI Journal, XXXVII (9). |

|---|---|

| ↑2 | AICPA FVS SSFS No. 1. Available at: Statement on Standards for Forensic Services | Resources | AICPA & CIMA |

| ↑3 | Duffus, David. (2019, August 27). “Overview of the statement on standards for forensic services.” Baker Tilly website. Available at: https://www.bakertilly.com/insights/overview-of-the-statement-on-standards-for-forensic1 |